- On May 13, 2025

- EBHRA, HDHP, HSA

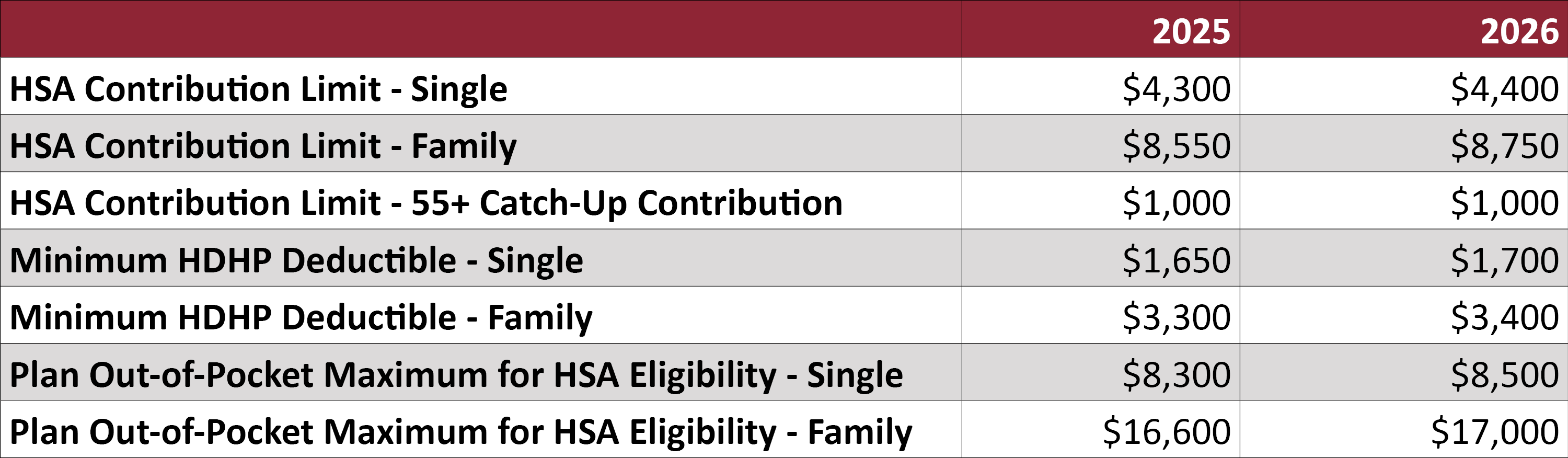

The IRS recently released Revenue Procedure 2025-19, which contains the 2026 limits for HSAs and high deductible health plans (HDHPs).

Qualified individuals with self-only coverage will be able to contribute $4,300, a $100 increase from 2025. Qualified individuals with family coverage may contribute up to $8,750, a $200 increase from 2025. As always, individuals aged 55 and older may make an additional $1,000 catch-up contribution. To be eligible, individuals must be enrolled in an HDHP with a minimum deductible of $1,700 for self-only coverage and $3,400 for family coverage. The maximum out-of-pocket expense limit will increase to $8,500 for self-only coverage and $17,000 for family coverage.

The IRS also released the inflation-adjusted limit for excepted benefit health reimbursement arrangements (EBHRAs) for plan years beginning on or after Jan. 1, 2026. Effective for 2026 plan years, the maximum annual employer contribution for an EBHRA will increase to $2,200 (up from $2,150 for plan years beginning in 2025).

EBHRAs

An EBHRA is a relatively new type of employer-funded health care account that reimburses employees tax-free for their eligible medical expenses. Employers can use EBHRAs to supplement their traditional group health plan coverage and help employees with their out-of-pocket medical expenses, including deductibles, copayments, and coinsurance amounts.

Employers of all sizes may offer EBHRAs. Although an employer must offer a traditional group health plan, employees are not required to enroll in the employer’s group coverage (or any other type of coverage) to be eligible for the EBHRA.

As an excepted benefit, an EBHRA is not subject to the same compliance requirements that apply to traditional HRAs. For example, EBHRAs are not subject to the Affordable Care Act’s market reforms or HIPAA’s portability rules. However, the EBHRA must be made available to all similarly situated employees on the same terms, without regard to health factors. Also, an EBHRA cannot be used to reimburse premiums for individual health insurance coverage, group health coverage (other than COBRA or other group continuation coverage), or Medicare coverage.

Like other types of HRAs, EBHRAs are subject to ERISA unless an exception applies. This means that Form 5500 may be required, and participants should receive a Summary Plan Description of the EBHRA and its benefits. EBHRAs are also subject to HIPAA’s privacy and security requirements and the nondiscrimination rules for self-insured health plans.

Annual Contribution Limit

Only employers can contribute to HRAs, including EBHRAs. EBHRAs are subject to a maximum amount that may be made newly available for the plan year. This maximum amount is adjusted annually for inflation. These adjusted limits are as follows:

- For plan years beginning in 2025, the contribution limit is $2,150; and

- For plan years beginning in 2026, the contribution limit is $2,200.

This limit applies to each eligible employee, regardless of whether they have single or family health coverage. While an EBHRA may reimburse a spouse’s or dependent’s eligible medical expenses, the limit is not higher for employees with family members.